877.227.4484

877.227.4484

Life Settlement Laws, Regulations & State Licensing Requirements

Over the past decade, the laws and regulations governing life settlement transactions have changed as quickly as the life settlement market itself. Welcome Funds, Inc. employs a fully-staffed compliance department and in-house counsel to address all regulatory issues.

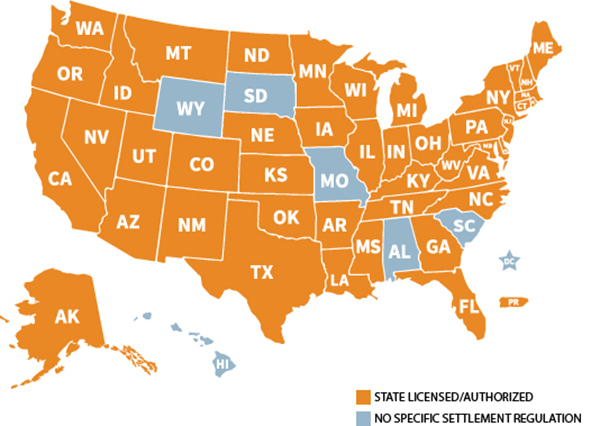

Welcome Funds and/or a principal of Welcome Funds is authorized, registered and/or licensed to conduct business in 45 states. In some cases, where state laws vary, Welcome Funds and/or a member of its senior management team is licensed as a viatical/life settlement broker and/or a life producer. In addition, we confirm the licenses of referring agents to ensure compliance prior to accepting and to finalizing a life settlement transaction. Please contact Welcome Funds for up-to-date licensing information.

Map updated December 2022

Life Settlement Applications

A life settlement application is a formal request to sell an existing life insurance policy for a lump sum cash payment. The purpose of a life settlement application is to allow policy owners to access the true value of their life insurance policy before it matures or before the insured person passes away. This can be useful for seniors who no longer need or can not afford their life insurance policy, or for those who are facing financial difficulties and need to access cash quickly.

Please select the state of residence of the Policy Owner and click to download our life settlement forms. If the Policy Owner is a Trust, then be sure to select the state in which the Trust is officially domiciled. It is imperative to use the proper state forms as disclosures vary by state and the transaction will be governed according to state viatical settlements or life settlement law in the Policy Owner's home state.

If you have any questions, feel free to contact us at 877.227.4484 for a complimentary Life Settlement Consultation or you can find out if you qualify for a life settlement using our Quick Life Settlement Qualifier - it's fast, easy and there are no obligations at any time.

Choose a State

- Indiana

- Iowa

- Kansas

- Kentucky

- Louisiana

- Maine

- Maryland

- Massachusetts

- Michigan

- Minnesota

- Mississippi

- Missouri

- Montana

Choose a State

LIFE SETTLEMENT BLOG

Direct Life Settlement Buyers vs. Welcome Funds – Advisor Beware!

Posted: by John Welcom

Welcome Funds has the privilege of working with numerous financial advisors and wealth managers – and have done so for two decades – some who exclusively focus on servicing high net worth clients. One such advisor who is active in the life settlement market — and already understands the value he can create for his clients — had historically negotiated directly himself with two or three leading buyers of life insurance policies. He thought that simply engaging with mor...

How to Sell Your Life Insurance Policy for $4,743,000 Instead of $275,485?

Posted: by John Welcom

Mr. Williams purchased $10 Million in life insurance coverage in 2001 to provide his family with financial security. Over time, his financial priorities changed: his wife passed away, his children became financially independent, financial burdens arose and the estate tax exemption increased substantially.

Suitability of Life Settlements

Posted: by John Welcom

Traditionally, estate planning advisors counsel their high net worth clients to obtain life insurance policies with large death benefits. The strategy is simple: create a vehicle for heirs to receive tax-free income at the time of an insured’s passing so sufficient funds are available to pay large estate tax bills when assets are inherited.

What is the Most Suitable Exit Strategy for Life Insurance?

Posted: by John Welcom

All eyes in the life insurance agency and the financial advisory world have been on New York, where in the summer of 2019, the New York State Supreme Court paved the way for implementation of Insurance Regulation 187. This rule imposes a new standard for agents and brokers when issuing a recommendation to a client regarding an annuity or life insurance product.

How to Get the Highest Life Settlement Offer

Posted: by John Welcom

When you decide to sell a valuable personal asset, you usually want to obtain the highest purchase price for that property. It is sound business sense. However, how do you truly know when you have reached the point of accepting and securing the most desirable offer?

Understanding the Fair Market Value of a Life Insurance Policy

Posted: by John Welcom

When a professional advisor identifies a life insurance policy that a client no longer needs or wishes to maintain, he should ask, as standard protocol, whether that policy may have value in the secondary market. If so, the client may be able to sell the policy in a life settlement transaction, enabling him to receive a higher cash payout than he otherwise would obtain by lapsing or surrendering the policy back to the insurance company.

The Power of a Life Settlement Auction

Posted: by John Welcom

Professional advisors with clients who no longer need or wish to maintain a life insurance policy have options when exploring the secondary market. Many advisors prudently rely on a licensed life settlement broker to assist them in the sale of the policy and with all aspects of the transaction. However, there is still a large number of professionals persuaded to work directly with only one buyer, called a life settlement provider.

Rebuttals to the “Direct Buyer” Model for Life Settlements

Posted: by John Welcom

Most professional advisors who explore the potential sale of an unwanted life insurance policy on behalf of their clients will rely on the assistance of a licensed life settlement broker. Life settlement brokers represent the policy owner in the transaction and have a duty to act in their best interests. Most notably, the broker’s and client’s goal is aligned: to sell the policy for the highest price possible.

Carrier Resistance To Life Settlements: Clients Need To Know They Can Sell Their Policies

Posted: by John Welcom

Consumers who sell their life insurance policies in the life settlement market receive as much as seven times more money than they would have received by surrendering their policies back to the insurance companies. Seven times! However, an estimated 9 out of 10 policies are allowed to lapse before paying a claim, according to the Life Insurance...

The Danger of Trying to “Time the Market” for Life Settlements

Posted: by John Welcom

Most investors in the stock market understand the danger of “market timing” — trying to choose the right day to buy a stock when the price is low and sell it when the price is high.